Charity investors navigating between different asset classes

Charity trustees are accustomed to dealing with uncertainty. However, when it comes to investment portfolios the current environment can feel particularly uncomfortable. Markets have been volatile, commentary is mixed, and assumptions that felt reliable over the past decade are being tested.

For many charities, the choice appears stark. One option is to remain heavily invested in equities and assume that long term trends will continue. The alternative is to move towards assets such as cash or bonds in order to protect capital, accepting that this may reduce future returns. Neither route feels entirely satisfactory.

It is worth stating clearly that trustees are not confined to these two choices. The Charity Commission permits investment across a wide range of asset classes, provided decisions are taken in the charity’s best interests and are supported by appropriate advice. There is no rule that portfolios must be limited to listed equities and bonds. The requirement is prudence, suitability and proper oversight.

The difficulty is that many trustees are comfortable with equities and bonds because they understand them. Other asset classes can feel unfamiliar, which naturally creates hesitation.

Why equities became the default

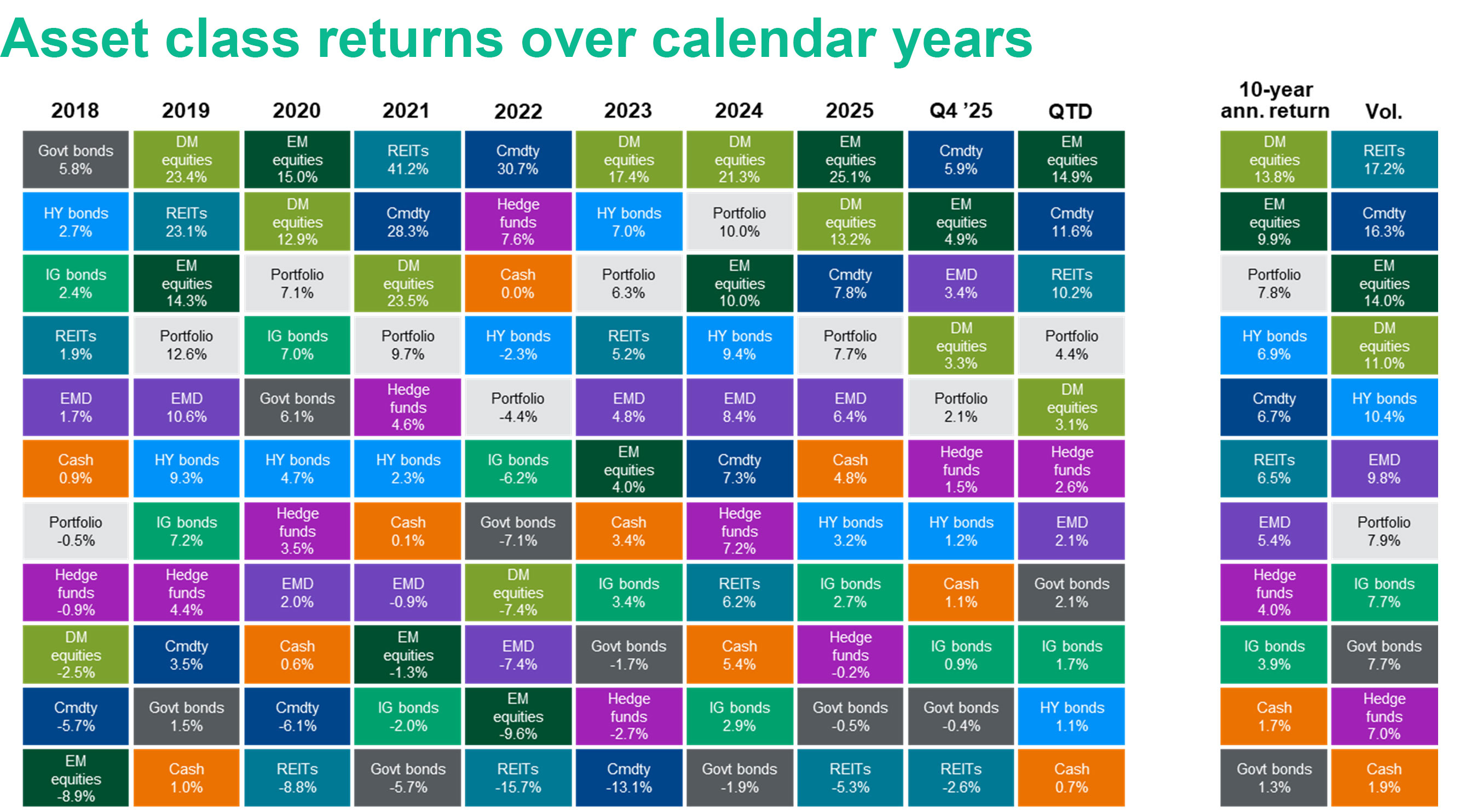

It is not hard to see why equities dominate many charity portfolios. Over the past decade developed market equities have delivered strong returns. This has been visible in performance tables year after year. Equities are widely discussed in the media, priced daily and comparatively straightforward to explain.

Trustees who increased equity exposure in recent years were responding rationally to the evidence available at the time. The issue now is whether that evidence still points in the same direction.

(Source: J.P. Morgan Guide to the Markets 30 Nov 2025.)

Markets look ahead, whereas investors often look back. Many portfolios reflect what has worked rather than what may work from today’s starting point.

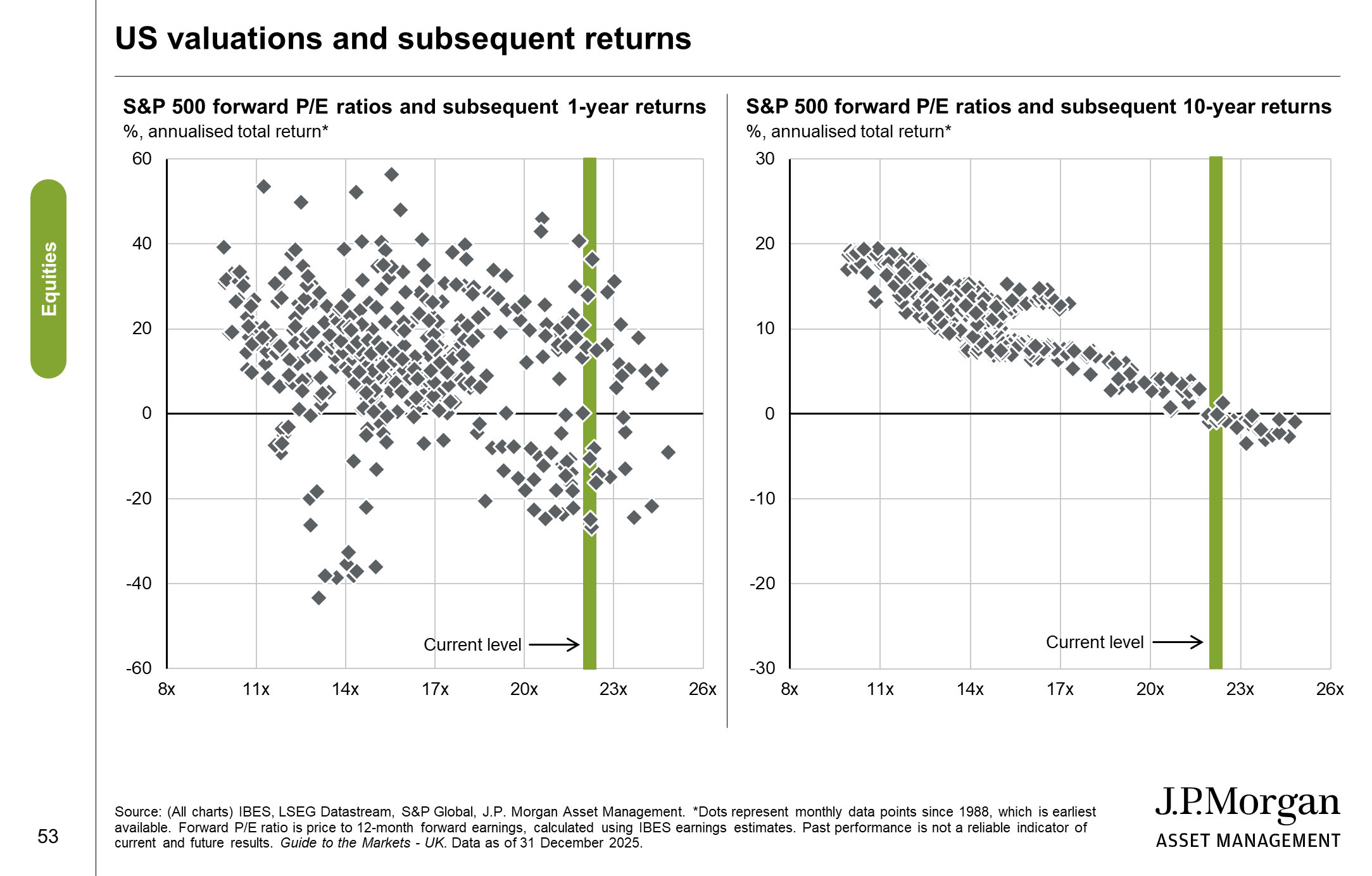

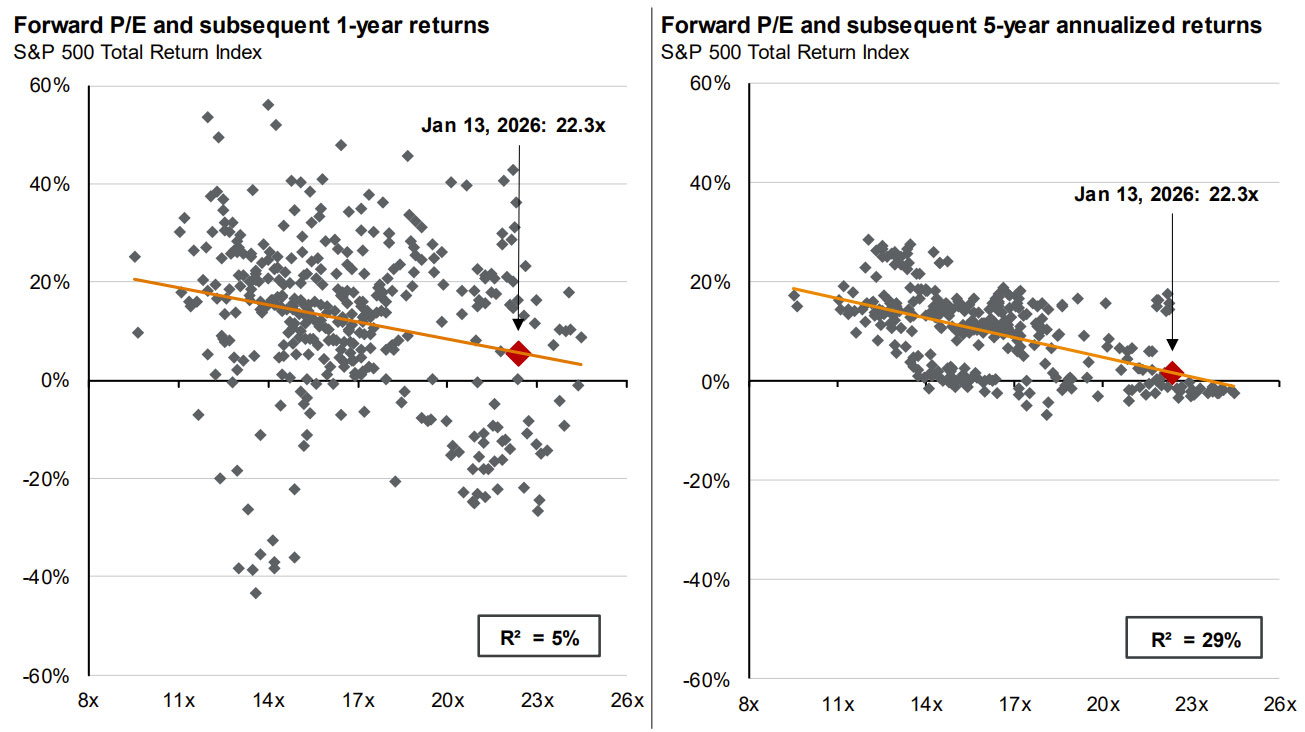

Valuations provide one way of thinking about this. Price to earnings ratios are not reliable guides to short term movements. Over longer periods, however, starting valuations have often influenced subsequent returns. Periods that begin with higher valuations have frequently been followed by more modest outcomes over the next decade.

J.P. Morgan – summary data as shown in the chart (including the bottom-line message on prospective returns).

Current equity valuations remain relatively elevated compared with long term averages. This does not mean that a correction is imminent. It does suggest that future returns may not match those experienced in recent years. Charities with very high equity allocations should therefore consider what a prolonged period of subdued returns would mean for their mission, especially when expenditure continues regardless of market conditions.

Looking beyond equities and bonds

If high equity exposure raises concerns, and cash and conventional bonds offer limited appeal, trustees may reasonably ask what else can be considered.

Charities are permitted to invest in a range of additional asset classes, typically accessed through regulated pooled investment funds managed by professional firms. Examples include:

- ASSET BACKED SECURITIES. These are investments backed by diversified pools of loans or receivables. Income is often linked to prevailing cash rates plus a margin.

- INFRASTRUCTURE ASSETS. These provide exposure to essential services such as energy, transport, utilities or digital networks, usually through diversified funds.

- PRIVATE MARKET ASSETS. This includes private credit and private equity, offering access to businesses and lending activity outside public markets.

For trustees who are used to equities and bonds, these areas can appear complex. It is important to understand how they are implemented and what they involve in practice.

How these investments are accessed

Charities do not typically invest directly in a toll road, a wind farm or a portfolio of individual loans. Instead, exposure is gained through collective investment vehicles. These may be authorised funds or limited partnership structures overseen by regulated managers.

Such vehicles pool capital from multiple investors and spread it across many underlying assets. Professional teams conduct due diligence, monitor risk and provide reporting. Trustees should expect clear documentation covering investment objectives, risk factors, liquidity terms, fees and governance arrangements. Independent custody and external audit are standard features of established funds.

The governance responsibility remains with trustees, yet day-to-day management and monitoring sit with experienced investment professionals.

Understanding the risks

Each of the asset classes mentioned carries distinct risks. Asset backed securities are exposed primarily to credit risk. Borrowers within the underlying pools may default. There can also be structural complexity. Diversification across large numbers of loans and careful credit analysis are used to manage these risks. Trustees should seek clarity on credit quality and stress testing.

Infrastructure investments can be sensitive to regulation, operational performance and economic conditions. Many assets provide essential services, which can support relatively stable cash flows. Diversification across sectors and regions reduces concentration risk. Trustees should understand the revenue model and regulatory environment.

Private market investments generally involve longer holding periods and less liquidity. Returns may be delivered unevenly. Valuations are typically updated periodically rather than daily. Trustees need to be comfortable with longer time horizons and should examine manager track records, alignment of interest and fee structures carefully.

In all cases, advisers should explain not only the potential return but also downside scenarios and how these investments fit within the overall portfolio.

Assessing performance

Performance assessment requires an appropriate timeframe. Unlike listed equities, alternative assets do not provide constant price signals. Infrastructure and private market strategies may need five to ten years to demonstrate results across a full cycle.

Trustees should judge performance against the stated objectives of the fund and the role it plays within the portfolio. Comparisons with global equity indices over short periods are unlikely to be helpful. The key question is whether the investment is delivering the income, diversification or return characteristics that were expected when it was selected.

Liquidity considerations

Liquidity is a central concern for charities. Funds are needed to support charitable activity, so access to capital matters.

Liquidity terms vary across funds. Some asset backed securities funds offer periodic dealing. Infrastructure and private market funds may have defined notice periods or lock up arrangements. In stressed conditions, dealing restrictions can apply.

This does not make such investments inappropriate. It does mean that liquidity must be managed deliberately at portfolio level. A balanced portfolio typically combines readily realisable assets with longer term holdings. Trustees should understand notice periods, redemption arrangements and worst case scenarios before committing capital.

Questions trustees should ask

If an adviser proposes allocating to these asset classes, trustees may wish to ask:

- What role does this investment play within the portfolio?

- How does it improve diversification or expected returns?

- What are the main risks and how are they controlled?

- What is the expected holding period?

- How liquid is the investment in normal and stressed conditions?

- How will performance be measured and reported?

- What are the total costs?

Asking these questions reflects responsible governance rather than resistance to change.

A balanced perspective

Equities are likely to remain an important part of most charity portfolios. The intention is not to replace one concentration with another. The aim is to ensure that portfolios are constructed with awareness of valuation starting points, liquidity needs and governance capacity.

Trustees are not required to embrace unfamiliar assets without understanding them. They are, however, permitted to consider a broader range of tools if doing so supports their charitable objectives.

In uncertain markets, thoughtful diversification, grounded in clear understanding and appropriate advice, may help charities navigate between excessive risk and excessive caution while remaining focused on their mission.